ESMA figures reveal disproportionate costs for HNW investors in UCITS

Chris Hamblin, Editor, London, 15 April 2020

The costs of dealing in Undertakings for the Collective Investment in Transferable Securities or UCITS are far higher in the European Union for retail investors than they are for institutional investors, according to a report released by the European Securities and Markets Authority. In some cases the difference is stupendous.

UCITS refers to conventional retail investment funds regulated and supervised in the EU. At just under €10 trillion in net asset value (NAV), it represents the largest retail investment fund segment in the European Union. Retail predominates, but the share of UCITS that ESMA thinks is being targeted towards institutional investors has been growing in recent years, from 27% on average in 2012 to 35% in 2017.

Costs throughout the asset classes are less variable for retail than for institutional investors and costs are on average higher for retail, which includes the HNW market. The difference in fund-related costs between retail and institutional investors is especially marked for bond UCITS, with cost affecting gross annual returns for retail bond UCITS by 1.3ppt and for institutional bond UCITS by 0.5ppt.

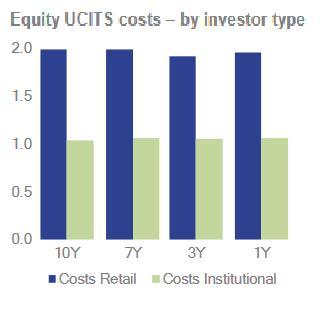

The main difference between UCITS sold to retail investors and the ones sold to institutional investors is the level of cost. For equity UCITS sold to retail investors (see diagram), the effect of continuing costs is around 1.9ppt (at 10-7-3-or 1-year horizons) compared with around 1ppt for institutional investors.

Regarding money-market-fund (MMF) and alternative UCITS, again the differences between retail and institutional investors remain. Costs for retail investors are higher by about 0.2ppt for MMF UCITS and 0.6ppt for alternative UCITS.

It is interesting to note that in some cases and over some time horizons, retail UCITS have slightly higher gross annual returns than institutional UCITS (as for equity at a 1-year horizon or bonds at a 7-year horizon). This pattern may indicate that 'liquidity needs' and risk-related considerations might weigh more heavily with institutional investors than with retail clients. Despite this, gross returns for retail and institutional UCITS still follow very similar patterns.

For institutional investors, again, the effect of inflation is significant but lower than it is for retail investors.

When ESMA looks at the size of UCITS retail markets by domicile by domicile for all investors, Luxembourg stands clear of the field.

The share of asset classes for UCITS marketed to retail investors by EU countries varies a good deal. In Belgium, Spain and Italy the share of mixed UCITS for retail investors is respectively 50%, 49% and 58% of domiciled UCITS in Q4 2017. In other domiciles the largest share is either taken up by equity (including Germany on 52%, the United Kingdom on 59% and Sweden on 60%) or bonds (Austria, 48%). There are other domiciles in which the largest share is held by both equity and bonds – in Luxembourg, equity accounts for 35% and bonds 34%; in Denmark the figures are 42% and 43%.

ESMA has lifted the data and the classification of UCITS by asset class, investor and management type from Thomson Reuters Lipper, an affiliate of Thomson Reuters. This American firm only counts funds as institutional if they declare themselves as such. The data is based on the domicile of every fund, not the domicile of every investor.